When Your Word Was Worth More Than Your Credit Score: The Era of Corner Store Tabs

When Your Word Was Worth More Than Your Credit Score: The Era of Corner Store Tabs

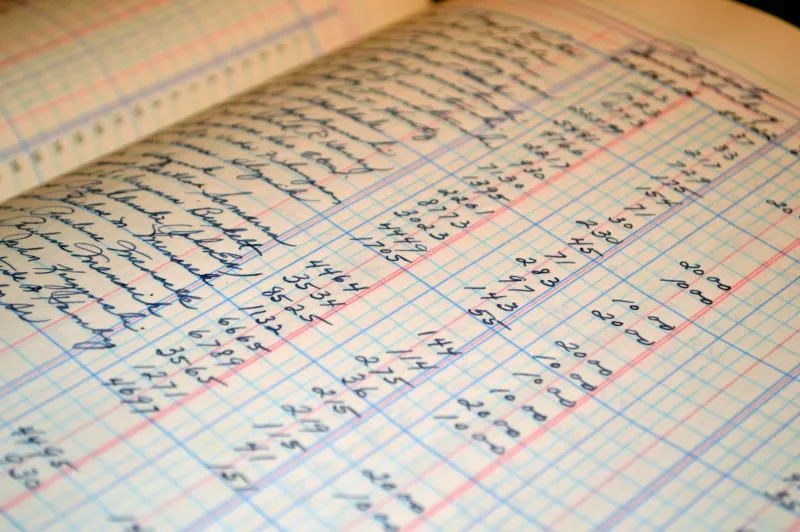

Picture this: You walk into Murphy's Hardware on Main Street, grab a hammer and some nails, and tell old Pete behind the counter you'll settle up on Friday when you get paid. He pulls out a worn ledger, scribbles your name and the amount, and sends you on your way with a nod. No card swipe, no credit check, no interest rate — just trust.

For most of the 20th century, this scene played out millions of times across America. The neighborhood tab wasn't just a convenience; it was the backbone of small-town commerce and a testament to something we've almost entirely lost: economic relationships built on personal knowledge rather than data points.

The Ledger Book Economy

Before the 1970s, running a tab at your local store was as common as stopping by the post office. Grocery stores, hardware shops, pharmacies, and even gas stations operated informal credit systems where regular customers could buy what they needed and pay when they could.

The system was elegantly simple. Store owners kept handwritten ledgers with customer names, purchase dates, and running balances. Some families had tabs at multiple stores — the grocer for weekly shopping, the hardware store for home repairs, the pharmacy for medicine. Payment schedules were flexible and personal. Farmers might settle up after harvest, factory workers after payday, and seasonal employees when work picked up.

What made this work wasn't paperwork or legal contracts — it was community knowledge. Store owners knew their customers' families, their work situations, their character. They knew who always paid eventually and who might need a gentle reminder. This wasn't just business; it was neighborly support disguised as commerce.

Trust as Currency

The tab system created bonds that went far beyond buyer and seller. When Mrs. Johnson couldn't afford her groceries during her husband's illness, the grocer didn't cut off her credit — he often extended it, knowing the family's situation was temporary. When young couples were starting out, store owners would often approve informal credit that no bank would touch.

These relationships created a social safety net woven through daily commerce. Stores became community institutions where people's financial dignity was preserved even during tough times. The phrase "good for it" carried real weight because everyone knew everyone else's story.

Store owners took pride in their judgment of character. Being trusted with store credit was a mark of community standing, and maintaining that trust was a matter of personal honor. Children learned about financial responsibility by watching their parents interact with storekeepers, seeing firsthand how reputation and reliability worked in practice.

The Death of the Handshake Deal

Several forces combined to kill the neighborhood tab. The rise of suburban shopping centers in the 1960s and 70s made commerce more anonymous. Chain stores replaced family-owned shops, and corporate policies replaced personal relationships. Credit cards, introduced widely in the 1960s, offered a more systematic way to extend credit.

But the real death blow was mobility. As Americans moved more frequently for jobs and opportunities, the deep community knowledge that made tabs work began to disappear. Store owners couldn't know every customer's background, and customers couldn't build the long-term relationships that made informal credit possible.

By the 1980s, most neighborhood tabs had vanished, replaced by credit cards, layaway programs, and eventually, the complex web of credit scoring and algorithmic lending we know today.

The Algorithm Knows Your Number, Not Your Story

Today's credit system is simultaneously more sophisticated and more impersonal than anything previous generations could have imagined. Your creditworthiness is determined by algorithms that analyze your payment history, debt ratios, and financial behavior patterns. A three-digit credit score carries more weight than decades of community standing.

Modern buy-now-pay-later services like Klarna and Afterpay offer instant credit decisions based on data analysis, not personal knowledge. You can get approved for a purchase in seconds, but the approval comes from a computer program that doesn't know if you're going through a divorce, caring for a sick parent, or between jobs through no fault of your own.

The efficiency is remarkable — you can buy almost anything on credit anywhere in the country. But something essential has been lost. Modern credit is purely transactional, stripped of the human context that once made financial relationships part of community life.

What We Lost When We Gained Efficiency

The old tab system wasn't perfect. It could be exclusionary, sometimes based on prejudice rather than fair assessment. It was limited in scale and couldn't support the complex, mobile economy we have today. But it offered something our current system lacks entirely: financial relationships that accounted for the full complexity of human circumstances.

When your local storekeeper knew your family history, your work ethic, and your character, credit decisions were made with context that no algorithm can capture. The system built community bonds and taught financial responsibility through personal relationships rather than penalty fees and credit score monitoring.

Today, we have more access to credit than ever before, but we've lost the human element that once made financial transactions part of the social fabric. We've gained efficiency and scale, but we've lost the neighborly trust that once made a handshake as good as a contract.

In an age where artificial intelligence makes split-second lending decisions based on vast data sets, it's worth remembering when your word was worth more than your credit score — and when the person extending you credit knew not just your payment history, but your story.